Energy, innovation, and growth

© TIM Garrett 2014

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

Available statistics show that wealth, when it is integrated over the entire global economy, and integrated over the entire history of economic wealth production, has been related to the current rate of global primary energy consumption through a factor that has been effectively constant over nearly four decades of civilization growth. The implication is that aggregated civilization wealth and consumption has inertia, and therefore its current growth rate is unlikely to cease in a hurry.

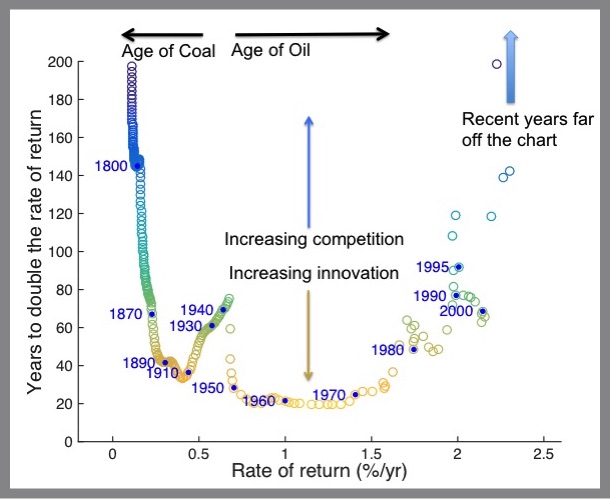

Adjusting for inflation, the time for a generalized measure global wealth to double its rate of return (calculated as a decadal running mean), shown versus the rate of return for wealth itself. The numbers can be applied equally to energy consumption. Select years are shown for reference.

Yet the global rate of return on wealth does change, even if slowly. Historical statistics shown in the figure above indicate that, over the past century or so, there has been a long term tendency for growing rates of return on global wealth. In the late 1800s, adjusting for inflation, rates of return for the total global economy were about 0.2% per year. Today, it’s about ten times higher: we double our collective wealth every 30 years or so. As a whole, the world is getting richer faster.

I use the word innovation to describe this acceleration of inflation-adjusted rates of return because it represents the capacity of civilization as a whole to beat mere inertia. Adjusting for inflation is important here, because it is not always evident that any investment in innovation will pay off. If investing in human creativity does not lead to true innovation, then it is a waste of effort. The investment could have otherwise contributed to maintaining previously attained rates of growth. But, real innovations provide a jump in rates of return that civilization can carry forward into the foreseeable future.

Globally, innovation has come in fits and starts. The figure above shows that innovation has had two golden periods over the past two centuries. The first was during the Gilded Age or “Belle Epoque” of the late 1800s and early 1900s, when resource expansion and technological discoveries allowed the rate of return to double in just 40 years. Then again, in the baby boom period between 1950 and 1970, the rate of return doubled in the remarkably short timespan of just 20 years.

By contrast, both the 1930s and the past decade have been characterized by much more gradual inflation-adjusted innovation rates. Even though wealth is now doubling more quickly than ever before in history, for the first time since the Great Depression the rate of return is no longer increasing.

Why has the passage of history been characterized by economic “fronts” on global scales, with rapid innovation giving ultimately giving way to stagnation?

Here again, physical principles can provide guidance. Given that inflation-adjusted wealth and energy consumption appear to be linked through a constant, the identical question is asking what enables energy consumption to accelerate.

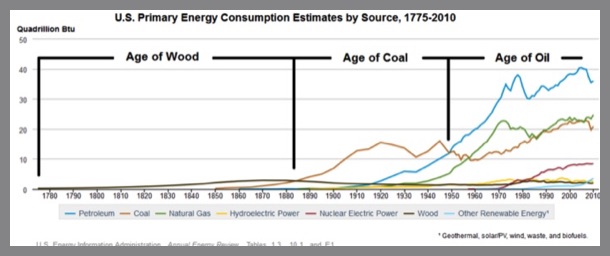

Conservation laws from thermodynamics tell us that rates of innovation and growth should be largely controlled by the balance between how fast civilization discovers new energy reserves and how fast it depletes them. For example, it is easy to imagine that access to important new coal reserves in the late 1800s and new oil reserves around 1950 allowed civilization to capitalize on human creativity in ways that were previously impossible.

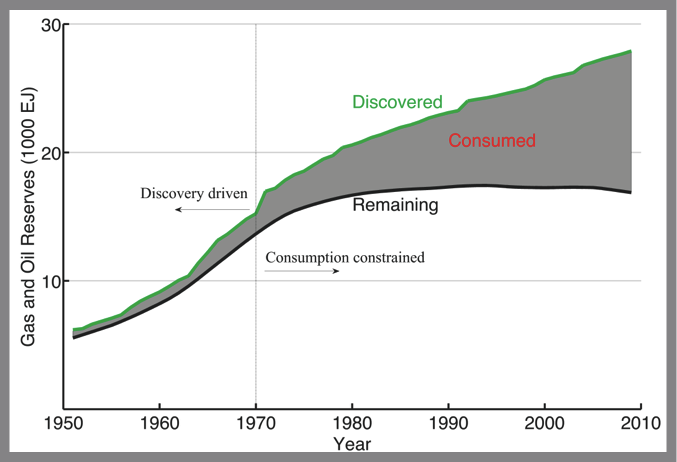

Today, we continue to discover new energy reserves, but perhaps not sufficiently quickly. We are now very large and we are depleting our reserves at the most rapid rate yet, just barely keeping pace with discoveries. Increased competition for resources may be constraining our capacity to turn our creativity and knowledge into real innovation and accelerated global economic growth.

Economics About Physics of the economy What is wealth?

Energy, Innovation and growth Economic inertia Economic Forecasting Jevons' Paradox

Physics vs Mainsteam Economics Is Macroeconomics a Science? The economic heat engine

Economics and Climate GDP is not Wealth Are renewables the answer?

Is population growth a problem? Will growth transition to collapse?

What is your carbon footprint? Media Publications Presentations FAQ Criticisms