A thermodynamic power theory of value

© TIM Garrett 2014

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

On the Physics of Wealth

What are the origins of wealth?

Economics textbooks describe wealth, value, or capital, as a physical “stock”. The value of this stock is sustained by our collective beliefs. The economy is made of physical stuff whose value is ruled by competing forces of supply and demand. Through labor, stuff can be used by people to produce more stuff so that overall wealth grows.

At least on the face of it, this view of the economy makes a lot of sense. Economists have mathematical equations that express these ideas providing quantitative descriptions for how and why the economy grows.

Yet something still seems a bit unsatisfyingly magical about this approach. It doesn’t actually explain in any truly fundamental way why we would believe in the concept of economic value in the first place, especially one expressible in units of currency. The existence of a financial system is hardly obvious. It hasn’t always existed through history, even during periods where people certainly produced and consumed. And most of our lives (fortunately) doesn’t involve any exchange of currency. We are able to enjoy a good moment of each other’s company without having to pay for it.

The economy and the second law

A clue to the economic puzzle is that there are overarching principles that govern everything. Sure, financial wealth is a human quantity, but we are still part of the physical universe. No matter how rich we may be, we are all equal subjects of its universal rules.

Chief among these rules is the Second Law of Thermodynamics. Unfortunately, the Second Law has been expressed in many ways that are either wrong, strangely mystical, or maddeningly vague. Perhaps the most straightforward and easy perspective is to view the direction of time as an overall flow of matter from high to low potential energy density or pressure. The flow of matter redistributes potential energy to ever lower values. Drop something it falls. It was up, now it’s down; air flows from high to low gravitational potential or pressure to make the winds. Absent a renewed external input, the universe “runs down”. Easy.

What does this have to do with the economy? Well, everything. Consider that we cannot measure the size of anything, even the value of some economic stock, without a perception of a flow. Any signal we measure flows from a high potential source to some lower potential where it’s sensed. For example, if you pay attention to someone or something, perhaps to assess it’s value, what is physically happening is that your brain uses energy to process a light contrast that flows down a potential gradient to the sensors in your eyes.

Perhaps more easily, take the waterwheel in a mill. The mill consumes high potential energy in a flowing stream. The flow sustains all wheel circulations before the flow finishes its journey in the stream below where the potential energy is dissipated and lost. The ability of the mill to dissipate this energy, its size or its “stock”, is something we can estimate by looking at the size of the mill and noting how fast it circulates.

So how do we generalize these ideas to assess the size of the stock of our global economy? This might initially seem like an enormously difficult question to answer: There’s 7+ billion of us, our brains are so complicated, and the economy is so big.

That is until we recognize that the flow that sustains civilization circulations is the consumption and dissipation of high energy density “primary energy resources”.

As a global organism, like these shipping vessels at an oil rig, our civilization collectively feeds on the energy in coal, oil, natural gas, uranium, hydroelectric power and renewables. Civilization continually consumes these resources to accomplish two things: the first is to propel all civilization’s internal “economic” circulations; the second is to incorporate raw materials into our structure in order to grow and maintain our current size against the ever present forces of dissipation and decay.

Energy, of all kinds, powers our machines, our telecommunications, modern agriculture, and the supply of the meals that give us the energy to sustain our thoughts, attention, and perceptions. Without energy, civilization would no longer be measurable. Everything would grind to a halt. Nothing would work. Lacking food, we would be dead and our attention span with it. The gradient that meaningfully distinguishes civilization from its environment would disappear. Value would vanish.

Thus, implicitly, our collective assessment of economic value reflects our combined estimation of an item’s capacity to facilitate global economic circulations through its connectivity with the rests of civilization. The more connected, the more something or someone facilitates dissipative flows, the more value that thing or person is.

Yes, some element of belief is involved here, or at least perception. But that’s the point. The key thing to recognize is that we ourselves are part of a much more general expression of global economic wealth than is traditionally assumed. Our brains require dissipative circulations as much as traffic circulations. Currency is just the psychological manifestation of an expression of value stated more physically in units of energy and time. Global circulations between and among us and our stuff are sustained by the rate of global primary energy consumption. Wealth is power.

Stepping back to see the world economy as a simple physical object, one where people are only part of a larger whole, would be a stretch for a traditional economist hung up on the idea that wealth must be restricted to physical capital rather than people. But, crucially, unlike traditional models, it is an idea that can be rigorously tested and potentially disproved. It is a hypothesis that is falsifiable. If the above is correct then we should expect to see that summing up the inflation-adjusted of GDP all nations, over the entirety of history, this very general expression of inflation-adjusted global economic wealth is tied to global primary energy consumption through a numerical constant, independent of the year that is considered.

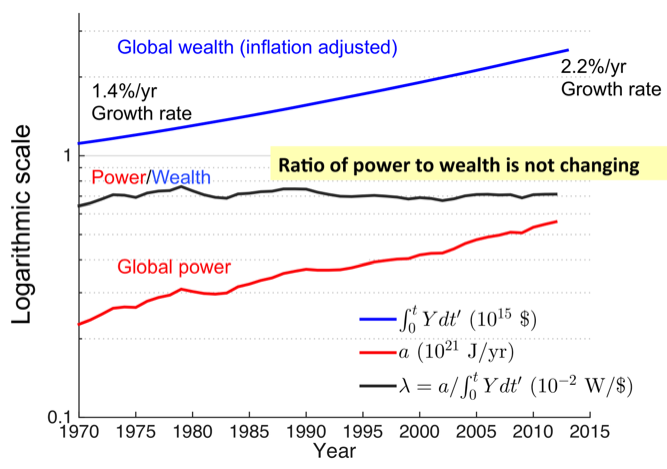

I have shown in peer-reviewed studies published in Climatic Change, Earth System Dynamics, and Earth’s Future that this simple hypothesis appears to hold true. The observed relationship between the current rate of energy consumption or power of civilization, and its total economic wealth (and not GDP), is a fixed constant of 7.1 ± 0.1 milliwatts per inflation-adjusted 2005 dollar. Equivalently, every 2005 dollar requires 324 kiloJoules be consumed over a year to sustain its value. The log-linear plot below shows wealth in blue, energy consumption rates in red, and the value of the constant in green. In 2010, the global energy consumption rate of about 17 TW sustained about 2352 trillion 2005 dollars of global wealth. In 1970, both numbers were about half this. Both quantities have increased slowly from 1.4% per year to 2.2% per year averaging a growth rate of 1.90% /year.

The above shows a measure of global wealth (calculated from the historical accumulation of world economic production, inflation-adjusted) and energy consumption. On a log-linear plot, both are growing nearly linearly, i.e. approximately exponentially with respect to time on a lin-lin plot. The rate of growth (the slope of the curve) has gradually increased over time, but has been about 1.90 %/year on average. The ratio of the two quantities has stayed nearly constant over a time period when both wealth and energy consumption have more than doubled and the rates of growth have increased by about 50%.

Note that the comparison here is not between energy consumption and physical capital or the global gross domestic product (GDP), as has been erroneously claimed in published criticisms of this work. Physical capital is just one portion of total civilization generalized wealth . And GDP has units of currency per time where wealth has units of currency. GDP and generalized wealth are not at all the same thing. Mathematically, wealth is defined as the time integral, or historical accumulation of inflation-adjusted world economic production.

Physics of the GDP

Finding a constant that ties economics to physics has some rather far-reaching implications. Among these is that, at global scales, the real (inflation-adjusted) GDP is determined by how fast civilization consumption of energy is growing.

The product of the global GDP and same fixed constant of 7.1 ± 0.1 milliwatts per inflation-adjusted 2005 dollar is, on average, the growth rate of energy consumption. Over long timescales (perhaps a few years to a decade), what this means is that we must continue to grow our capacity to consume primary energy reserves just to sustain the existence of a positive real GDP. The GDP growth rate that is commonly quoted is then related to the acceleration of energy consumption, or the growth rate of the growth rate.

We should never conclude that economic growth can’t continue over coming decades, as some claim in perennial doomsday predictions. It’s just that there is nothing stronger than inertia to guarantee that it will. The water wheel in the picture above can rot or the river can dry. Atmospheric high pressures can dissolve into low pressures. For us, continued consumption growth may quite plausibly become too difficult due to depletion of energy and mineral reserves or accelerating environmental disasters, for example from accelerating carbon dioxide emissions. If this happens, all our efforts to produce growth can be expected to be more than offset by decay.

At some point, all systems experience decay and collapse. Nothing grows forever, despite what economists say. And there is no such thing as a steady-state, at least not for long. We’ve seen the waxing and waning of civilizations throughout history.

Historical studies suggest that any long-term decline in a society’s capacity to consume forebodes hyper-inflation, war, and population decline. The question for us should not be whether collapse will happen, but when, and whether it will be slow or sudden. Here, I believe that applications of physics take forecasts of our future away from fairy-land fantasies of “expert opinion” and into the realm of robust hypotheses that are physically constrained and can be as rigorously tested as forecasts of the weather or climate.

Long run evolution of the global economy: 1. Physical basis, Earth’s Future doi:10.1002/2013EF000171

Long run evolution of the global economy: 2. Hindcasts of Innovation and Growth, Earth System Dynamics

Economics About Physics of the economy What is wealth?

Energy, Innovation and growth Economic inertia Economic Forecasting Jevons' Paradox

Physics vs Mainsteam Economics Is Macroeconomics a Science? The economic heat engine

Economics and Climate GDP is not Wealth Are renewables the answer?

Is population growth a problem? Will growth transition to collapse?

What is your carbon footprint? Media Publications Presentations FAQ Criticisms