GDP is not Wealth

© TIM Garrett 2014

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

These pages argue for there exists a fixed relationship between energy and wealth, that there is a constant number that ties global rates of energy consumption and the time integral of inflation-adjusted economic production, a sum across all nations and a sum across all years since the beginnings of civilization. The motivation for calculating Wealth I have is outlined here and in the supporting material for this article:

Long run evolution of the global economy: 1. Physical basis Supporting Material, Earth’s Future doi:10.1002/2013EF000171

The time integral of real GDP is a totally different quantity from GDP, I call it Wealth simply because it has units of currency rather than currency per time, recognizing that traditional economic models have a more restrictive terminology of wealth based purely on physical capital. Call it something different if you prefer. The important thing is that the annual GDP may appear to have units of dollars, but this is only because it is the accumulated production over an arbitrarily defined period of one year. The generalized wealth described here, on the other hand, is the accumulated production over all of civilization’s history, where annual real GDP can be best understood as the yearly averaged inflation-adjusted addition to wealth.

Expressed in the terms of calculus, production is the derivative with respect to time of wealth, or wealth is the time integral of production. Time integrals and their derivatives are as independent as speed and acceleration. At any given time, they are unrelated. This is (or at least should be) clear whether traditional equations are used or the substitute I’ve proposed. Still, I have have consistently heard economists talk about time integrals of quantities and the quantities themselves as if they were effectively the same thing, or at least linearly related. This is very, very wrong, or at least only right for the very special case of constant exponential growth or decay.

For example, the following peer-reviewed paper introduced a physics based economics model that defined wealth very generally as the totality of civilization, including people, and provided theoretical and empirical arguments showing that wealth is tied to civilization’s rate of energy consumption.

Garrett, T. J., 2011 Are there basic physical constraints on future anthropogenic emissions of carbon dioxide? Climatic Change 104, 437-455, doi:10.1007/s10584-009-9717-9

Two commentaries accompanied the above article in the journal Climatic Change, both solicited by the chief editors Michael Oppenheimer and Gary Yohe. These critiques were not peer reviewed. From Is accurate forecasting of economic systems possible? by Irene Scher and Jonathan Koomey

“Believers in an unbreakable link between energy use and GDP assigned the immutability of physical law to this historical relationship (just like Garrett does) but found their belief shattered by events”

From Psychohistory revisited: fundamental issues in forecasting climate futures by Danny Cullenward, Lee Schipper, Anant Sudarshan and Richard Howarth

“Essentially, Garrett is saying that there is a fixed ratio of energy inputs to economic outputs, and that all plausible visions of the future will follow this relationship. This perception is sorely mistaken on both theoretical and empirical grounds.”

“Indeed, the trend we observe in the data—a declining energy/GDP ratio—would seem to be the counterargument to Garrett’s model formulation”

“...the evidence to date shows that the global E/GDP ratio has been steadily declining over the last 40 years; the available data do not support the theory that the ratio has been constant.”

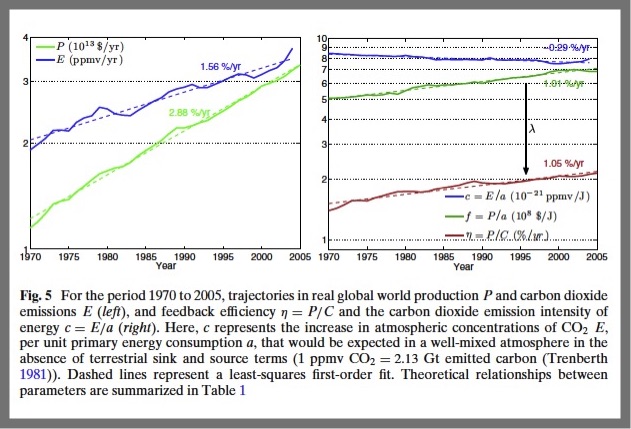

To show why these statements are so strange, the article I wrote is based on the relationship of energy consumption to wealth being fixed while it makes quite detailed arguments that the energy/GDP ratio is changing and explores reasons for why. Even the abstract states that energy productivity varies with time, where it is defined as the ratio of GDP to energy consumption. Figures showing evolution of this or a thermodynamically related quantity are shown in Figures 3, 4, and 5 (see the green line on the right below). There, and in Table 1, the rate of change is explicitly given as about 1% per year, which bizarrely is the same trend Cullenward et al. argued for in their effort to dismiss my article. Section 6 is almost entirely devoted to a detailed discussion of how the ratio changes, and the article conclusion states “For predictions over the longer term, what is required is thermodynamically based models for how rates of energy efficiency evolve.”

To recap: global wealth and GDP are not the same thing. One is the time integral of the other. They do not have the same relationship to energy consumption at global scales. Even in a hypothetical situation where inflation-adjusted global GDP were declining, wealth would still increase. Things would still be produced (hence the P in GDP). Since production adds, even if it is at a low rate, wealth would still grow. Even where the ratio of energy consumption to GDP is declining, the ratio of energy consumption to wealth remains a constant. Evidence for one is cannot be used as counter-evidence to the other.

Economics About Physics of the economy What is wealth?

Energy, Innovation and growth Economic inertia Economic Forecasting Jevons' Paradox

Physics vs Mainsteam Economics Is Macroeconomics a Science? The economic heat engine

Economics and Climate GDP is not Wealth Are renewables the answer?

Is population growth a problem? Will growth transition to collapse?

What is your carbon footprint? Media Publications Presentations FAQ Criticisms